In December 2024, in response to the press/advocacy campaign by Marc Andreessen and other crypto advocates regarding a phenomenon they call debanking, I wrote Debanking (and Debunking?) in Bits about Money.

That piece is the definitive explanation of the issue. It examines many angles including:

- the constraints on banks and their incentive structures

- how AML regulation sometimes hurts innocent entrepreneurs

- a detailed history of Operation Choke Point

- a detailed analysis of why two crypto-affiliated banks closed

- what the crypto industry hopes to win through the press/advocacy campaign.

Debanking (and Debunking?) won wide acclaim for being accurate, incisive, and balanced. Experts who publicly praised it include the crypto VC who coined the phrase “Choke Point 2.0” (“… the best and fairest treatment of the issue [I] could expect from a skeptic…”) and a former federal banking regulator (“This is a tour-de-force. This is absolutely excellent. Anyone interested in this issue should read this piece.”).

I am notoriously a crypto skeptic, but I do believe advocates have some points which are just true about debanking, a phenomenon which is much larger than crypto. They also have some arguments which deserve a fair hearing. They also say some things which are untrue and will not get more true simply by being strategically convenient.

You can’t please everyone

In many years of writing for the Internet, I’ve gotten my fair share of negative comments. It happens; oh well. Sometimes randos use cliches like “Delete this post.” These are easy to ignore.

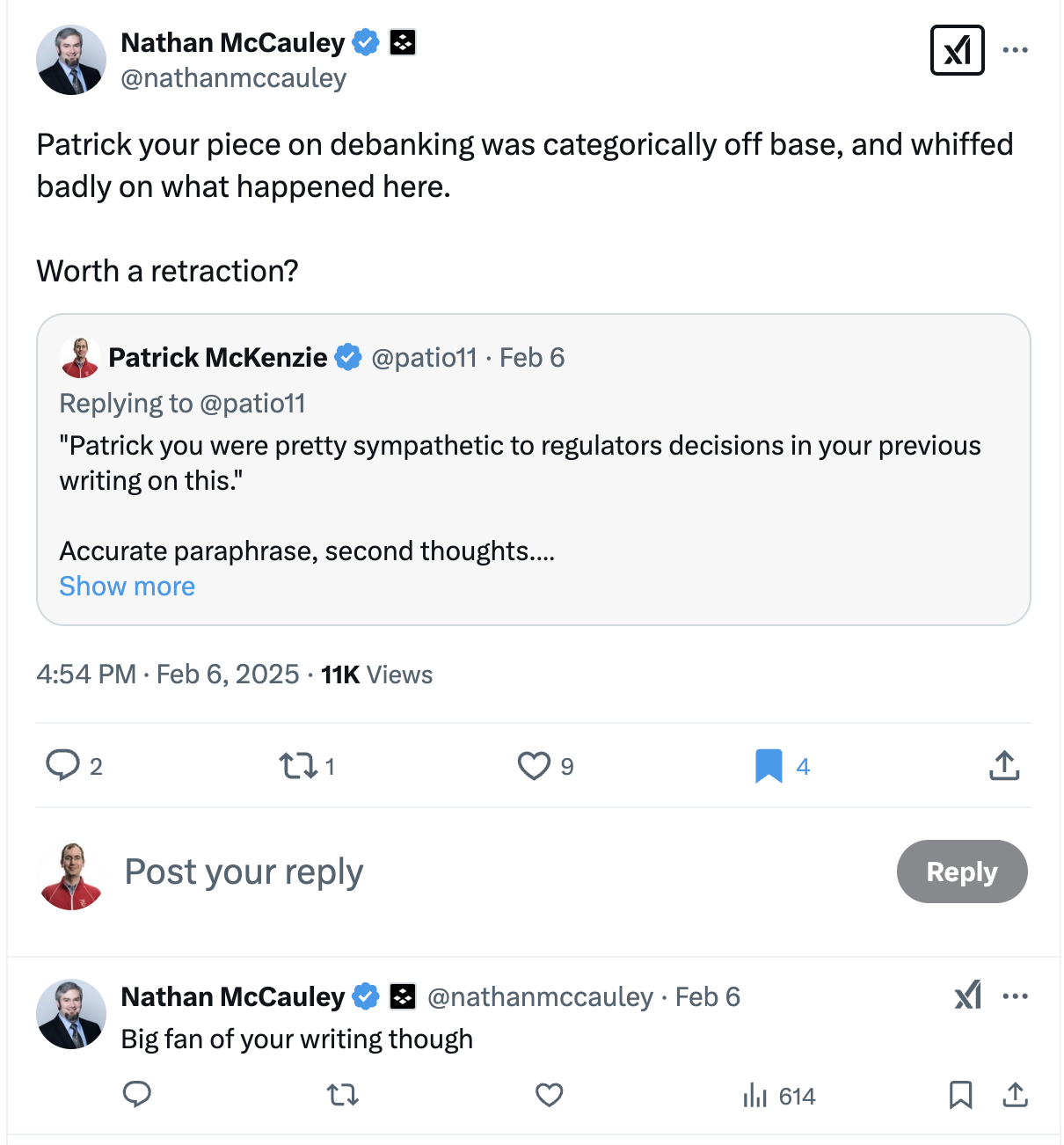

I recently received a request for retraction from a bank CEO. (Tweets sometimes become unavailable.) That is a first, and it deserves careful attention.

Bits about Money is a reader-supported professional journal about the intersection of finance and technology. It has been my primary professional output and source of income for the last two years. It generally takes pains to avoid antagonizing specific banks, in part because banks can be prickly about their reputations. But there was always a risk, in writing candidly about banking, that a bank or banker could react with severe displeasure.

Bits about Money is, like most of my professional writing, published by Kalzumeus Software, LLC. The following is in the voice of the company.

Nathan McCauley, the CEO of Anchorage Labs, Inc. d/b/a Anchorage Digital, and a board member (and, on faith and belief, CEO) of a federally chartered bank, has requested a retraction of the piece Debanking (and Debunking?). He alleges inaccuracies, misleading statements, omission of key facts, and other improprieties.

This is a serious allegation, and we treated it seriously. We have undertaken a review of McCauley's points. This review included requesting input from Anchorage Digital's PR team, reviewing the text of the published essay, and consulting with our external advisors.

We find McCauley's allegations to lack merit. We therefore decline to retract the essay.

The bar for a retraction is high

Retractions are, in the standard practice of journalism, research and other professional writing, extremely rare. They are reserved for the worst offenses: plagiarizing, fabricating quotations or data, committing libel, and the like.

I publish analytical essays about complex systems, and mostly do not break news. One is welcome to one’s opinion as to whether that counts as journalism.

I have a high regard for the truth. If I ever wander into error about the thing readers pay me to be an expert about, I try to correct the record. My preference is strongly towards corrections rather than retractions, as I have never unpublished a piece, but I would do it if warranted.

I have considered, and asked external advisors, whether it is possible that the CEO of a tech startup valued at over $3 billion might be unaware of what the word “retraction” means or that asking for one is a serious act. We unanimously concluded that I am entitled to assume the professionalism and competence of a founder of a tech unicorn or a bank CEO. McCauley is both.

Because the specific allegations made do not show the professionalism and competence of the speaker in a positive light, I reached out to Anchorage Digital in advance of publication, via their PR department’s published email address. I asked, among other things, if they had reason to believe their CEO’s Twitter account was compromised. There is always a risk that someone is signing one’s name to stupid letters without authorization.

Anchorage Digital’s PR team did not reply to my request for comment, despite receiving three emails and a clearly communicated timeline which was longer than one business day. As Anchorage Digital itself tagged McCauley’s account the day prior on the occasion of his testimony in front of the U.S. Senate Banking Committee, and did not identify his account as compromised, I treat the authenticity of his messages as a settled question.

I will take the charitable perspective that a tech founder and bank CEO does not necessarily speak for the startup and/or bank themselves. Anchorage Digital knows my email address if they would like to clarify this or any other point.

Our review of the retraction request

On receiving the request for retraction we reached out to McCauley to ask what specifically he believed was inaccurate in the piece. This was also an opportunity for McCauley to recharacterize his request as, for example, an indelicately phrased expression of personal opinion.

McCauley did not respond by walking back the request for retraction. Instead, he replied with what he seems to believe constitutes a litany of improprieties. As he has numbered his subpoints, we will address them in turn.

McCauley:

A few areas were incorrect and misleading, lots of omission of key facts, and missing the point about what we mean by debanking.

In order:

1. “A few areas were incorrect and misleading”

McCauley:

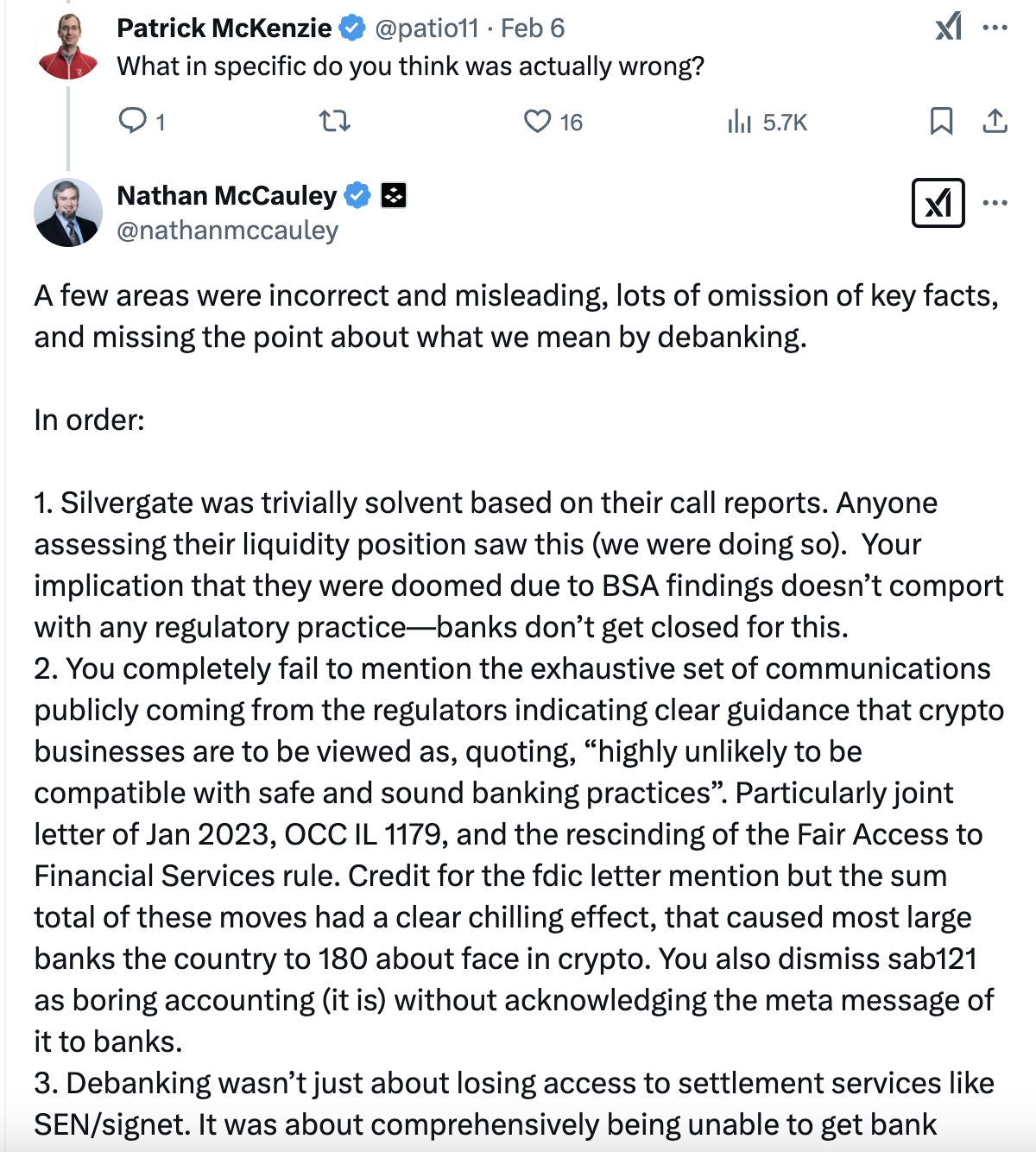

Silvergate was trivially solvent based on their call reports. Anyone assessing their liquidity position saw this (we were doing so). Your implication that they were doomed due to BSA findings doesn’t comport with any regulatory practice—banks don’t get closed for this.

Our response regarding solvency: Had we stated or implied that Silvergate was insolvent, that would have been very improper. Insolvency of a financial institution is a serious charge. We assume McCauley believes we must have made it, because no bank CEO could possibly believe that solvency is the only obligation of a financial institution.

We did not make this accusation.

We reviewed the 4,300 words written about Silvergate specifically, and cannot identify any statement which can be reasonably read as alleging insolvency. A reader who wanted to quickly verify this might use Ctrl-F “solv” (three hits in the piece, none about Silvergate, and one expanding to “solving”). One could also run the piece by an expert in banking practice, who might point out the following is persuasive evidence of solvency.

Debanking (and Debunking?):

Silvergate voluntarily liquidated in the wake of the FTX implosion. Limited props for them here: they managed to do this in a mostly orderly fashion, as opposed to Signature, which had substantially less crypto exposure but blew up.

If one’s bank does not employ an individual who understands the above paragraph to mean that Silvergate was solvent, Anthropic will sell you artificial cognition for $20 a month. Claude 3.5 Sonnet demonstrates sufficient reading comprehension to analyze complex technical documents to the standards of an early-career employee in financial services. We would recommend supervising Claude with management at least as competent as it.

Our response regarding Bank Secrecy Act (BSA) findings:

We have reviewed our writings with respect to Silvergate’s broadly deficient BSA compliance regime, including the anti-moneylaundering (AML) errors it made. We stand by the entire analysis, most particularly the conclusion, which we did not articulate lightly.

Silvergate was not a competently run institution.

We charitably assume that Anchorage Digital has mandatory training regarding BSA/AML compliance. This is required of all banks. McCauley has even more reason to be familiar with this requirement than the typical bank CEO.

McCauley and Anchorage Digital Bank, National Association are signatories to a 2022 consent order with the Office of the Comptroller of the Currency (OCC).

That consent order stems from the OCC’s finding that, quoting the order:

As of 2021, the Bank failed to adopt and implement a compliance program that adequately covers the required BSA/AML program elements, including, in particular, internal controls for customer due diligence and procedures for monitoring suspicious activity, BSA officer and staff, and training.

We have no particularized knowledge as to what Anchorage Digital’s internal training instructs employees regarding the range of sanctions available for non-compliant behavior. If that training does not rhyme with every other training in the financial industry, we suggest Anchorage Digital might consider updating it.

(We gave McCauley and Anchorage Digital’s press team days of advance notice of our intention to mention the consent order. We gave them the opportunity to provide a comment regarding it. Neither offered a comment.)

Debanking characterizes the standard training thusly:

If you’ve worked in the financial industry in any capacity, you went to mandatory Compliance training. Attendance is taken and you likely had a refresher annually. And there were smirks, and jokes. And your trainer said, very seriously, “Pay attention. This is important. If we eff this up, they can do anything to us, most likely large fines but up to and including closing this firm. You, personally, could go to jail.”

Banks are, of course, welcome to their own risk analyses, and may consider the risk of being closed for AML/BSA compliance violations to be very low. This point of view appears common among crypto bankers. Silvergate executives have professed to share it.

As mentioned in Debanking, closing a bank is an extraordinary remedy, but it is on the table.

Case studies which might enliven one’s next training include:

- Farmington State Bank d/b/a Moonstone Bank (2023): closed by the Federal Reserve because it was puppeted by a coalition of Tether’s bankers, who are as-yet unindicted professional money launderers, and Sam Bankman-Fried et al, who are now-convicted professional money launderers.

- ABLV Bank (2018): designated an Institution of Primary Money Laundering Concern and forbidden from using dollar clearing, resulting in the European Central Bank effectively directing Latvia to close it, which Latvia did.

- Washington Federal Bank for Savings (2017): closed by the OCC for a control fraud, BSA violations, and other malfeasance. The senior executives and directors were sanctioned individually and several went to prison.

- FBME Bank (2017): designated a Financial Institution of Primary Money Laundering Concern by FinCEN. It was liquidated as a direct and intended consequence.

- Banca Privada d’Andorra (2015): designated a Foreign Financial Institution of Primary Money Laundering Concern by FinCEN. It collapsed as a direct and intended consequence.

Summary: McCauley fails to identify an incorrect allegation of fact made by Debanking. Viewing his statements in a light most favorable to him, he disagrees with our analysis. He is welcome to articulate his point of view in his own spaces, the bank’s spaces, or the halls of the Senate. He is not entitled to a retraction.

To the extent McCauley believes that any respectable publication would retract over this, he is greatly miscalibrated. We could end the inquiry here, because his next two bullet points do not even purport to allege inaccuracies, but we will continue.

2. “lots of omission of key facts”

McCauley:

You completely fail to mention the exhaustive set of communications publicly coming from the regulators indicating clear guidance that crypto businesses are to be viewed as, quoting, “highly unlikely to be compatible with safe and sound banking practices”. Particularly joint letter of Jan 2023, OCC IL 1179, and the rescinding of the Fair Access to Financial Services rule. Credit for the fdic letter mention but the sum total of these moves had a clear chilling effect, that caused most large banks the country to 180 about face in crypto. You also dismiss sab121 as boring accounting (it is) without acknowledging the meta message of it to banks.

We concur that the Joint Statement on Crypto-Asset Risks to Banking Organizations (of the Federal Reserve, FDIC, and OCC, in January 2023) was an important milestone. Which is why we cited it as such. It was linked in the following discussion.

Debanking:

Banking regulators get to weigh in on proposed banking products. That is the absolute core of the job. That will extremely routinely result in saying something which rounds, like many of the letters do, to “We are going to have a considered think about this and get back to you, but in the meanwhile, please don’t roll this out widely.” (The think was had; the results were published. Many crypto advocates do not like those results, and are asserting procedural irregularities because of that.)

The piece extensively argues that, contra the claims of crypto advocates generally (and McCauley in his testimony before the Senate after the piece was published), the publication of extensive written guidance (which we linked to) militates against concerns that these actions are, quoting McCauley’s testimony, “opaque [and] unfair.”

Debanking:

Conversely, when the government is capable of publishing extensively researched position papers and extensively footnoted indictments, that should give you more confidence that it is less likely to be engaged in lawless, arbitrary behavior. Not limitless confidence, certainly, but it is evidence in a direction.

Our response regarding SAB121: McCauley is the CEO of a technology company with a custody business and a foothold within the regulated financial perimeter. We are extremely aware of why he has a particular interest in SAB121.

While this accounting arcana is material to his firms’ business interests, we judged it of only tangential interest to most readers. We only gestured at it to (accurately and fairly) identify changing SAB121 as a policy goal of the crypto industry. It has since been rescinded.

McCauley’s apparent dissatisfaction with the discussion of SAB121 asserts no inaccuracy and is accordingly not a reasonable grounds for retraction.

3. “missing the point about what we mean by debanking”

McCauley:

Debanking wasn’t just about losing access to settlement services like SEN/signet. It was about comprehensively being unable to get bank accounts after those banks were closed. It was about banks we’d been working with for years kicking us out of the blue - and this happening across the whole industry.

Far from “missing the point” of what crypto advocates mean by “debanking”, Debanking points out that crypto advocates are engaged in strategic conflation of different issues. We could not have, at the time of publishing the following, known that McCauley would request a retraction using this strategic conflation, pretending (a word we do not choose lightly) that advocates do not really care about bank supervision, and only want business checking accounts.

Debanking:

Advocates often invoke a user-centric perspective of debanking, focusing on the impact on individuals/firms. Then, they conflate it with regulators’ decisions regarding bank supervision, in ways which are facially not about direct user impact.

Crypto advocates routinely exaggerate the universality of banks’ treatment of crypto. As Debanking discusses extensively, we absolutely agree with advocates that crypto companies have, at times, routinely experienced banking friction. If one is demanding a retraction, though, it pays to be precise and not use words like “comprehensively” to mean “not comprehensively.”

For example, as McCauley admitted in his testimony to the Senate Banking Committee, Anchorage Digital did find a banking partner.

Debanking, (following a discussion of our own two debanking incidents):

That is the typical end to a debanking story. “And then, I opened a new account.”

McCauley asserts, in his testimony, his belief that “over forty banks” would not have rejected Anchorage Digital but for regulators pressuring banks to cut off services to the crypto industry.

We have no specific knowledge about Anchorage Digital’s relationship with its former bank or more than forty prospective banks, and will let the common factor in those discussions describe them.

Quoting McCauley’s testimony to the Senate:

One day in June 2023, we received an urgent email from the bank informing us that they needed to speak with us that day. On the call, we were told that our account would be closed in thirty days because they were not comfortable with our crypto clients’ transactions. We attempted to explain the source of all payments from our crypto clients were fully documented as a part of our robust KYC, AML, sanctions compliance, and other internal transaction monitoring and attribution processes, and that we would be willing to provide more information to their risk management team. They were uninterested. They refused to engage in further discussions, provide any additional explanation, or offer any chance to appeal the decision.

Alongside this experience, we found ourselves shut out of the banking system at other touchpoints. After the closure of some of the few banks that were willing to serve crypto clients in March of 2023, we were forced to find a new banks [sic] to hold clients’ cash funds in custody for trading purposes, as well as an account to hold segregated regulatory capital, both required to be held at an FDIC-insured bank under the terms of our bank charter. Again, we should have been a desirable, low-risk client for a bank. Yet over the course of a seven month period we spoke to over forty banks and were rejected by all of them. Many did not even cite a reason; others just vaguely told us it was not within their risk appetite to work with crypto clients.

Our response:

We trust McCauley’s representation that this happened.

We also believe Debanking adequately explains to a non-involved individual why it happened. See the section Debanking specifically for AML risk. Indeed, a reader of Debanking would have, months before McCauley’s testimony, been able to predict elements like the 30 day notice period, the disinterest in further negotiations, and the lack of appeals process.

McCauley, like many crypto advocates, professes to believe that a legitimate crypto company is a low-risk bank client. His testimony discusses the desire of Anchorage Digital to have demand deposit accounts, on its own behalf and on behalf of customers.

We empathized in Debanking with crypto entrepreneurs who are not banking experts. Some might not understand how a legitimate, legal business could be anything other than a low-risk bank client. We explained how. At substantial length.

Crypto advocates love a bit of risk, and love even more when somebody else has to buy them out of the downside, while they keep the upside. The demand that banks just give them deposit accounts is a demand that bank shareholders backstop their credit (and other) risk. Crypto advocates mostly do not intend to give their banks equity for this risk.

One can understand how a crypto founder who is raising their seed round might not yet be a banking expert.

Members of a bank board of directors, on the other hand, are charged with managing a variety of risks to their bank. They must be able to articulate how a legitimate business could pose credit (and other) risk to a bank with only demand deposit accounts.

This topic is discussed extensively in Debanking, including a worked example from the experience of Metropolitan Commercial Bank. Metropolitan primarily provided “low-risk” cash management services to Voyager Digital, a cryptocurrency platform/exchange. Voyager was a legitimate business, publicly traded, and believed to be well-capitalized. It represented to its bank, investors, and regulators that it had best-in-class risk and compliance programs in place.

Voyager blew up, due to its best-in-class risk program seeing single-name exposure to $666 million representing 60% of loan book / 30% of all assets and leaping at the opportunity. When it collapsed, customers who had sent Voyager money, but not received crypto in return, began to initiate reversals of those transfers. Metropolitan was faced with a credit loss large enough to imperil their entire crypto banking practice, which was approximately a quarter of deposits prior to the collapse. Metropolitan was dragged into Voyager’s contentious bankruptcy. It was sued over its conduct and alleged lapses.

One wonders whether Metropolitan, in clarity of hindsight, considers providing cash management services to an upstanding cryptocurrency platform to be “low-risk.”

Metropolitan attributes “the strategic assessment of the business case”, along with the regulatory environment, for deciding to fully exit crypto banking, which they claim they had pivoted from beginning in 2017.

McCauley’s assertion that Debanking ignores a constellation of regulatory activity which caused the banking industry to update negatively on its view of crypto is unsupported and unsupportable. We analyzed it extensively, along with the other reasons the banking industry negatively updated on crypto.

McCauley’s concluding remarks

McCauley:

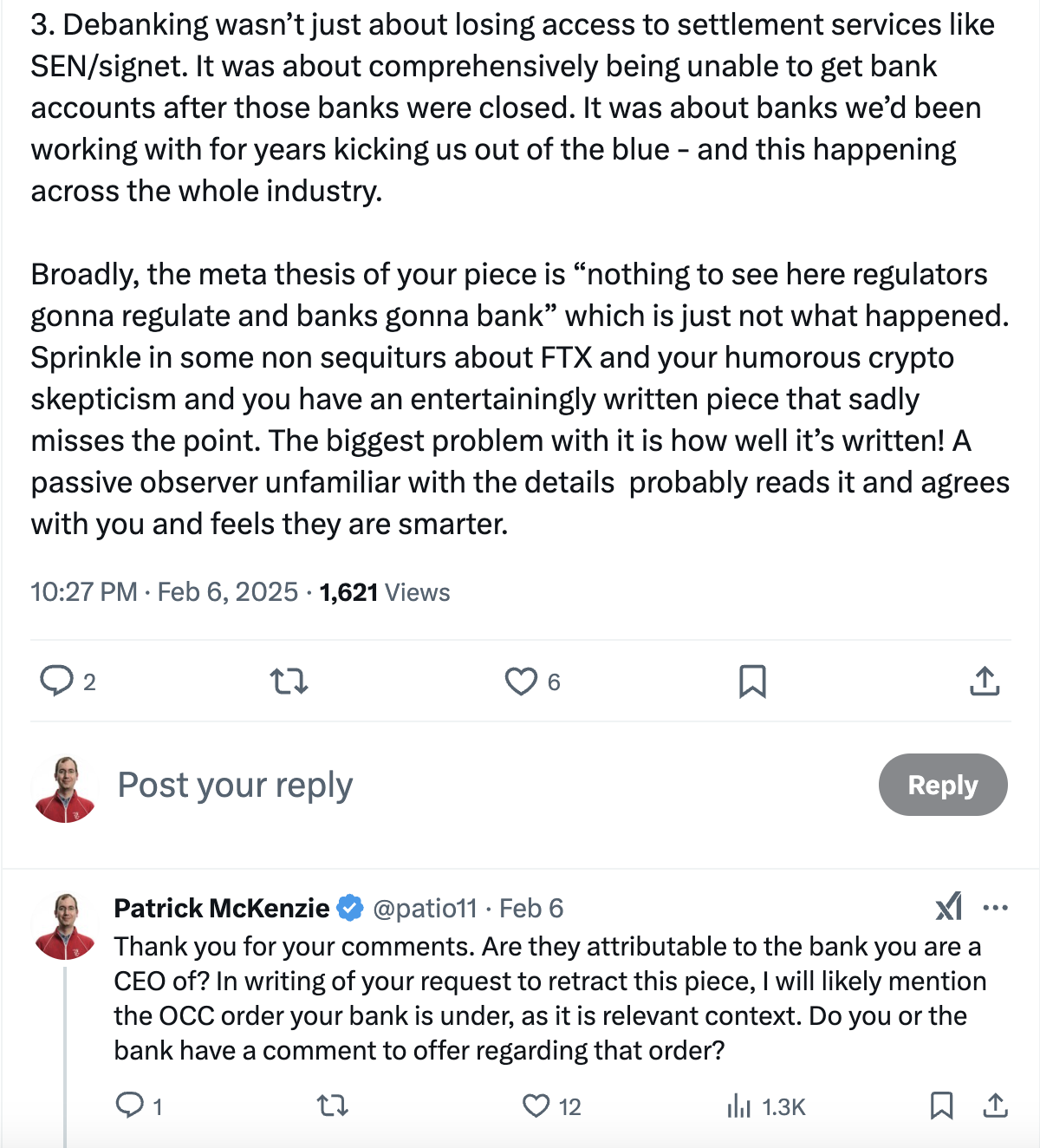

Broadly, the meta thesis of your piece is “nothing to see here regulators gonna regulate and banks gonna bank” which is just not what happened. Sprinkle in some non sequiturs about FTX and your humorous crypto skepticism and you have an entertainingly written piece that sadly misses the point. The biggest problem with it is how well it’s written! A passive observer unfamiliar with the details probably reads it and agrees with you and feels they are smarter.

McCauley misinterprets the thesis of the piece, which is hinted at in the usual place and in the usual manner: stating it explicitly, very near the top.

Debanking:

“It’s not a conspiracy theory if people really are out to get you.” sums up part of my reaction to [the claims of crypto advocates], but only part. There exists some amount of conflation between what private actors are doing, what state actors have de facto or de jure commanded that they do, and which particular state and political actors have their fingers on the keyboard. These create a complex system; the threads are not entirely divorced from each other.

We concur with McCauley that many readers might, after reading Debanking, feel that they are better informed about debanking than if they simply trust the representations of crypto advocates. Kalzumeus Software does not consider this a bug and WONTFIX.

We disagree with McCauley’s characterization of readers moved by the piece as “passive observer[s] unfamiliar with the details.” Many of our readers are extremely professionally invested in these topics, perhaps by dint of working in finance, financial technology, bank supervision, policy roles in the U.S. federal government, or the cryptocurrency industry.

McCauley has failed to identify a single fact alleged in Debanking which is incorrect, or any other malfeasance. Differences of opinion or different preferences in emphasis are, of course, not a reasonable basis for retraction. We accordingly reject his request for a retraction.

Bank CEOs do not often ask writers for retractions

I need to promote an important subtext to text.

It is exceedingly rare for bank CEOs, who are chosen for probity, sound judgement, and professionalism, to demand retractions. It is rare enough for banks to do it, and when they do, it usually follows quiet outreach by e.g. PR or Legal teams.

Some might mismodel writers as being thrilled by unprofessional behavior.

The incorrect model is that the writer immediately enjoys the opportunity to embarrass someone, and probably gets paid to do it. There is an old saw about “Never pick a fight with someone who buys ink by the barrel”; a more modern articulation might mention the Streisand Effect. (Wow, more than 20 years old now?! There are bank employees too young for that reference. Yeet it into an LLM if you need to.)

These bits of folk wisdom do not match how serious professionals perceive the incentives and power dynamics at play here. Banks are, as a class, much better resourced than writers (and almost all publications).

I am a very atypical writer vis the financial industry.

- I have substantial experience and expertise in the topics I write about.

- I have substantial resources and independent decisionmaking authority.

- I would take perverse joy in being sued by a crypto company.

Most writers work for an institution, and that is a Faustian bargain. On the one hand, working for an institution means that when a bank sues for libel, they will sue your employer, and not you. On the other hand, one’s Legal department, being very sensitive to the expense and annoyance of being sued for libel, will tread very lightly around prickly institutions and individuals. This includes exercising prior restraint of reasonable reporting and commentary.

A demand for a retraction by the CEO of a well-resourced financial institution is reasonably read by most outlets as being backstopped by potential legal consequences if they do not comply. Well-calibrated professionals understand retractions will only happen in the event of serious malfeasance. Accordingly, a request for a retraction is a statement that one believes one has suffered serious malfeasance.

Not all CEOs are well-calibrated. But publishers have to take certain genres of statements from certain genres of business owners much more seriously than other people might take them.

This includes when those statements are communicated via the Internet. The Internet is real life. A statement made by a bank using the Internet is a statement by a bank. Of course it wasn’t transmitted by telegraph, stagecoach, or carrier pigeon! A statement made by a bank CEO, etc etc.

And thus the recital above that e.g. Kalzumeus Software, LLC was and is the publisher of Debanking (and this piece), and thus the serious discussions with professional advisors. While I sometimes feel like I am LARPing at running a business, the great state of Nevada, the bank holding my mortgage, the IRS, and my insurance company are unanimous that I do in fact run a business. I am obliged to operate it in a competent fashion, including taking my legal responsibilities seriously, and managing risk to the business and other stakeholders.

Perhaps some bank CEOs feel like they’re just LARPing sometimes. I can empathize. But, to quote U.S. District Court Judge Ana Reyes (in a hearing on FDIC’s recent tussle with Coinbase), “welcome to the NFL.”

I speak only for myself and, as I’ve said for years, I work for the Internet. The Internet is humanity’s crowning achievement. It is also a community and that community has norms. One of those norms is that it fights attempts at censorship. As an Internet-native independent writer who is better resourced than almost all writers who will ever get a saber rattled at them by a bank or banker, I will say what they cannot.

This conduct is unwarranted, unprofessional, and dishonorable. It should cease.

The opinions, on the other hand, are merely wrong. One is welcome to publish one’s opinions to the Internet in a manner of one’s choosing. (One may have stricter obligations with respect to representations made to one’s regulators or e.g. Congress. Ask one’s lawyers.)

Some context regarding custodial banks

Many readers might wonder why a bank needs a bank. Indeed, McCauley’s verbal statement to Congress has a mic drop moment where he expresses incredulity that a federally chartered bank could be debanked. It’s great theatre.

A fun bit of banking Compliance trivia: there exist banks which one cannot bank at.

Anchorage Digital Bank, National Association is one such bank.

Quoting Anchorage Digital’s home page’s fine print:

“Anchorage Digital” refers to services that are offered through the wholly-owned subsidiaries of Anchor Labs, Inc., a Delaware corporation.

Anchorage Labs, Inc. is a tech company, and not a bank. That tech company has a relationship with Anchorage Digital Bank, National Association. That relationship involves receiving fees from the bank for services. As to whether it is an ownership relationship, well, I’d bet their lawyers can tell you a scintillating and true story about bank holding companies.

Anchorage Digital Bank, National Association makes much of the fact that they are a federally chartered bank, operating under the auspices of an agreement with the OCC.

Quoting Article V of their operating agreement with the OCC:

The Bank shall limit its business to the operations of a trust company and activities related or incidental thereto. The Bank shall not engage in activities that would cause it to be a “bank” as defined in section 2(c) of the Bank Holding Company Act.

Those activities? Taking deposits and making loans, the traditional business of banking.

Anchorage Digital was previously a trust company in South Dakota prior to getting the OCC charter.

Trust companies, a type of regulated financial institution, can run custody businesses. A custodian maintains legal and operational control of an asset, but does not own it. The owner pays them because keeping that asset safe and useful increases the value of the asset by more than the cost of custody. You are yourself, reader, very likely a beneficial owner of assets held at a custodian. This is especially likely if you hold financial assets which are not cryptocurrency tokens. You have probably not paid an invoice for these professional services directly. Another entity, such as e.g. your brokerage or a fund you are invested in, paid for them as a prerequisite to offering you a bundle of services, of which custody is one necessary component.

A custody business might have other modern products such as e.g. a real-time settlement API. That is one of Anchorage Digital’s marquee products. For a fuller discussion of real-time settlement APIs and why the crypto industry considers them structurally important, see Debanking’s discussion of the Silvergate Exchange Network.

Speaking of crypto trust companies, remember Prime Trust? It was a Nevada chartered trust company, which also had a custody business. Prime Trust purported to be the adults-in-the-room bilingual-in-TradFi eagerly-complying-with-regulations crypto custody company. They were going to clean up the cowboy behavior in the industry. This is a familiar sales pitch, also made by FTX, Voyager, BlockFi, Genesis, and probably some firms which are still with us, too.

Prime Trust lost a portion of the assets they were custodying due to technical incompetence (they wrote seed phrases allowing recovery of private keys on a piece of metal… then lost the metal). They then misappropriated other customer assets to buy substitute assets to fund withdrawals. This, per their bankruptcy filing, resulted in insolvency which they concealed from their regulators and customers through intentional fraud.

When this came to light, they were closed by their regulators. This was in June of 2023. By coincidence, that is the same month that Anchorage Digital lost their banking partner.

This loud and notorious collapse of a major competitor to Anchorage Digital, happening as a result of incompetence and malfeasance, despite that competitor having said all the right things, as part of a pattern, seems relevant to the interests of banks in the summer of 2023. One might choose to recount it in describing those banks’ reticence to do business with one’s industry. Perhaps one might acknowledge that one’s prospective banks might have had legitimate concerns. (Washington professionally appreciates a well-executed limited hangout.) Having done so, one might tease out the nuance that those concerns might have been surmountable but for excessive regulatory pressure.

Time is precious in front of elected officials, though, and Anchorage eschewed that and stuck to simpler messaging.

Anchorage Digital mentioned its strong commitment to seeking (direct quote) “the highest level of regulatory scrutiny and certainty”, and its determination to meet the obligations it has signed up for. This was repeated multiple times for emphasis.

At approximately 1:08:30 in the recording of the Senate hearing, CEO McCauley stated “That’s right. I’m a bit of a square, and like following rules, and so we always followed all the rules and regulations.”

I am also a bit of a square. I have never signed a consent order with the OCC regarding deficiencies in my bank’s BSA/AML program, however.

My business cards do say “wire transfer compliance influencer”

McCauley’s testimony that Anchorage lacks the ability to facilitate customer wires to third parties, “a basic banking service that we previously had access to”, may have surprised some listeners.

Readers of Debanking might be able to predict what point of view a sub-custodian bank might have regarding AML risk of third-party wires for crypto clientele. The sub-custodian might not be moved by a valued customer’s complaints their customers are simply crypto-native and traditional institutions requesting wires to crypto-native counterparties.

Why not?

For example, readers might remember the statement (quoted in Debanking, on the basis of reporting by Nic Carter): Where we were not as buttoned up as we should have been was in regards to the FTX/Alameda clients. That was a function of the bank growing incredibly quickly[.] … Probably we could have figured out FTX was brokering deposits via Alameda. In retrospect I think we could have pieced this together and figured it out.

Readers are welcome to their estimate of whether the quoted Silvergate executive, who Carter granted anonymity to, will work in banking again. Executives at many other banks do not relish the possibility of waking up to news that a crypto company was, once again, not as buttoned up as it should have been.

Returning to our regularly scheduled programming

As I point out in Debanking and elsewhere, crypto advocates would prefer to be judged on their potential rather than their track record. As a sometimes resident of Washington put it memorably: “What can be, unburdened by what has been.”

Optimism about future potential is highly prized in the startup community. It does not require unpublishing true claims about track records.

I continue to agree with crypto advocates on many of their claims. I will continue writing about the reality, warts and all, of the financial system. I will explain how history, humans, policy decisions, and technology have come together to deliver it. I will cover upgrades we’re collectively trying to build for it.

When those systems confound our expectations, or when their regulators are disregulated, interested readers will find facts and fearlessness in Bits about Money.

{kind=link}

{kind=link}

{kind=link}

{kind=link}